Housing Funding & Financing

Segment 1

Hello, and welcome to Affordable Housing Toolkit for Local Officials: Fundamentals of Funding and Financing. I'm Robin Wolff, Director of Rural Housing at Enterprise Community Partners, and I'll be leading this training today.

Segment 2

The goal of today's session is to introduce you to affordable housing finance basics and how you, as elected officials, can support the development of affordable housing in your communities.

Segment 3

With that, let's get to the basics.

Segment 4

One thing we want to discuss is how for-sale and multifamily rental housing can both be restricted for affordability. Well, it can also utilize similar financing sources funding that comes from HUD or USDA, or the Division of Housing's housing development grants, or the Federal Home Loan Bank's HP program.

Segment 5

When we're looking at financing for rental housing, we're thinking about how rents account for income, not from sales. We're also thinking about the size and the term of the loan that we're getting for construction and for permanent debt. The developer is generally earning their developer fee based on the closing of the transaction during milestones and at the end of the financing period, and initial close at the end of development. There's also, maybe, later, earnout for property cash flow that can also come back to the developer, owner, or operator. The entire interim financing is really repaid all together and the terms lenders source for payment is going to be coming from your net operating income, again, not on sales.

Segment 6

Question is: how does that work with for sale housing finance? Sale prices for for-sale are the revenue source to pay for development costs and developers getting to earn their fee at each component or each sale of the project. So, for example, if you have an infrastructure loan that's paying for sidewalks for five houses at the same time, that is going to be one loan, that then is written into the total development cost and the loan or the mortgage for each individual house. As you sell the house, that loan will get paid off and that will be the increments where that financing is paid off. So, the structure is slightly different, but we can still put it into a financial pro forma model. So, we can think about how the timing of sales needs to be projected and what we need to do in order to effectively get to where we want to be and to pay off our financing.

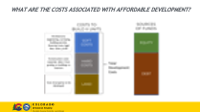

Segment 7

So, what are the costs associated with affordable housing development and how do we determine those? You might hear categories such as 'soft costs' or 'hard costs.' Soft costs include services such as architecture, engineering, surveys, building permits, financing costs, legal fees, and even taxes. Construction costs are going to be part of hard costs, as are things like materials and labor. Land is often put into a separate category all itself. The three of those together add up to your total development costs. How do we find our total development costs? On the right, you'll see we've got equity and debt. Basically, it's a combination of equity and debt that helps us to get to our sources that are going to pay for our total development costs.

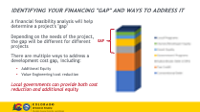

Segment 8

As we get started with development, we conduct a financial feasibility analysis. Through this analysis, we'll come up with what we call 'the gap.' The gap is the difference between the debt and equity you have currently in the project and what the total development costs for the project are actually going to be. So, in this example, as you see to the right of this slide, you've got a capital stack that includes local programs, owner-developer equity, grant equity... maybe that comes in from the State Division of Housing or from another government program... again, that could be coming from a source like the State, also could be coming from things like vouchers or programs that might exist in that space. Subordinate debt might come from a Community Development Financial Institution or another source that can provide secondary financing. In this example, we have tax credit in the stack as well (that's the orange), and then conventional debt--tax credit equity, you also come in on the equity side. You see, if you had a development where you had debt, and then you have some equity, there might still be a big gap, right? And that's where you're going to look to local programs, owner-developer equity, additional grants that might help you fill that. One other thing that could happen is value engineering that also can help you reduce your gap, meaning reduce the size of this stack or the size of this bar in this graph. That will reduce your gap as well. So, those are things that you could look at and, as a local elected official, you could play a role in both the cost reductions (thinking through fees and permits and costs that could help to decrease the gap on a project) and also as a source of funding for additional equity.

Segment 9

Let's think through how that would look for a for-sale project. And a for-sale project, we might use aggregate loan sizing, and we think of the defined starting limitations. For a $2 million loan, if you're going to build 20 homes, they will each cost $100,000. We have a clause in our loan agreement that limits the maximum number of houses that could be allowed at any given time to 10 houses. That is going to be coming from our debt finance or our bank that's giving us our loan. The other option is to use a revolving line of credit. That revolving line of credit may be for less money, let's say a million dollars, and the loan for each house will still equal $100,000. It means that you could build 10 houses under construction at any one time, and use that revolving line of credit as your first house sells. Then, you could work on your 11th house. As the second house sells, you'd work on your 12th house. That is the model for how we would structure our for-sale housing financing.

Segment 10

So, a for-sale feasibility analysis or gap analysis is going to look much like this. It will have your uses, design services, your general contracting fee, your materials, your financing, fees, development fees, and then you're going to have your cost per unit and your total units that you're building. All of this is going to be built into your financial analysis tool for for-sale development. You're also going to be thinking through your sources, the conventional loan in this case or in this example. The amount of equity or money that you might have put in or came through from a state or local program, for example, would be equity there. And then, you'll have your total development costs. As we can see on this slide, the gap here right now is $734,374. That is, comes up in this spreadsheet as your gap and will need to be made up either with equity or through value engineering.

Segment 11

Let's go back to our multifamily rental capital stack and think more about how we can create one for our individual project. So, the capital stack is the funding or investment structure of a project. Often, as we approach multifamily rental housing, we will need a stack or several sources in order to get to our total development cost. When we structure this, we think about the bottom of this stack as having the first priority for repayment, and then the softest or unencumbered funds are going to sit at the top of the capital stack. The reason is, those are going to be the last to get paid out in the case or event of a foreclosure or default. Equity in the project for that reason is really attractive, and that attracts funders to come in at that senior or more risky debt level.

Segment 12

Next, we're going to go to financial feasibility analysis and look more closely at the multifamily rental pro forma.

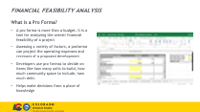

Segment 13

So, what is it pro forma and why do we use it? A pro forma is really a tool or a series of tools that helps us to understand the overall financial viability of a project. This kind of tool will be used by developers, and it'll also be used from an underwriting standpoint as we look at it as a new affordable housing development. It's going to assess a variety of factors including your operating expenses, it's going to look at unit size, think about rental income that can be derived from each typology or each kind of unit, and then help to determine what your net operating income is. Developers use these to determine how many units to build and how much community space to include. And also, to determine what amount of debt you can take on at the end. Understanding the pro forma helps us as developers and helps everybody who's involved in affordable housing development come to the decisions about what is created from an informed place.

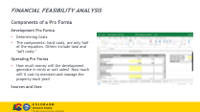

Segment 14

Let's talk through the components of a pro forma. This pro forma on this slide is modeled after the pro forma from the Division of Housing. Through the development pro forma, we can determine cost. So, those costs are going to have the hard costs and also those soft costs that we talked about previously on an earlier slide, and land acquisition. All of that should be part of that development cost tab on your pro forma. Another tab on your pro forma is going to be the operating pro forma, and that is going to help you understand how much money the development is going to generate in rents. If we're talking about a for-sale pro forma, the operating pro forma will come from a for-sale basis and rotational basis, as we saw previously in the slides earlier.

Segment 15

So, there are many things to keep in mind as we develop a pro forma. There's a lot of jargon: there's DSCR or debt service coverage ratio, NOI or net operating income... We talked about loan terms, amortization schedules. A lot of that can really be illuminated by looking at a pro forma tool and better understood through this analysis. Also, it's important to keep in mind that building a pro forma is iterative. You might start off with a project that's all three-bedroom units and understand that three-bedroom units may or may not be a great source or a great need in your market, and then you'll come back to your pro forma and change your unit mix. That unit mix change will then, in fact, change your rental income which then will affect change an NOI and your ability to take on debt. Those are all things to be factored in and they can be understood better through a pro forma tool. For that reason, don't wait until you're applying for money from the state or from another source and then, before, you put something into a pro forma. Use this tool early on to really understand what the balance is between your market needs and your availability to gain the sources needed to create your total development costs. It's a very important tool to start out early with and to keep going back to throughout your development process.

Segment 16

So, as you fill out your pro forma tool, you'll see the development pro forma and that will have questions about land acquisition and site acquisition costs. This is where you might need to think through whether or not you have a long-term ground lease or a different structure for land acquisition. You'll also have fees for planning and design and approvals, which will include specialists and market analysts and all of those other specialists that are going to work on the project. Site work and building construction is part of your cost structure. And then, amenities and off-site costs are also in need to be considered as you think through your total development pro forma. Not to be forgotten are your construction management and developer fees. All are important sources and costs that are coming into the project.

Segment 17

So, now we're at the operating pro forma. And really, the operating pro forma is a place where we can start to begin to balance our debt and our income. So, the operating pro forma can calculate things like your per unit per annum or PUPA expenses, and the amount of revenue the project will generate overall. And then again, the amount of income that will be available, let us know the amount of income that is available that will service our debt or the pay for our debt. So, things to think through as you're looking at your operating pro forma: Are you aiming to serve multiple income brackets? If so, how have you tiered rents, or have you tiered rents? That needs to be factored in to this pro forma and reflected in your operating income pro forma. Are you looking to serve varied sized households? Meaning, do you need four-bedroom units or three-bedroom units or a mix of three twos and ones? That also will affect this operating pro forma and there is a way to include all of those different factors and all of the different rents in this tab of the pro forma. Project-based vouchers are something else to consider. If you are looking to serve a large population of folks that aren't in under 30% income, that would limit your income ability in terms of generating revenue unless you have project-based vouchers. If you have project-based vouchers, those vouchers will cover the differential between what those folks can pay at an affordable rent level and what is available to them based on the voucher. So, something else that's really important as we're developing our pro forma. Other things that need to be understood as we're filling this out is your fair market rents in your area and the fair market rents for each type of unit size that you're looking at developing within your project.

Segment 18

So, now we're going to be assessing the permanent financing sources tab of our pro forma and understanding what permanent financing is going to be part of this project, and putting all of the information that creates your capital stack into the spreadsheet form. The permanent financing that will be included in this form include: conventional debt, which we talked about, generally as a first mortgage; secondary debt, which is a second or third mortgage (tertiary debt); tax credit equity would be in here; government grants; other grants, meaning grants that are not from a government entity and don't come with the government or compliance restrictions that come with government grants; and then owner equity, and that can be in the form of money that you're putting in the project and leaving as a project or it could be in the form of something like deferred developer fee. That will all be factored into your permanent financing sources. This is also where you understand and can assess what is the gap. Again, this is a workbook and a series of tools that works together. And as a consequence, you have to fill out your operating pro forma and your permanent financing pro forma in order to fully understand where your gap is at the end of this page.

Segment 19

Now that we've found the gap, we got to figure out how to fill it. So, this is about finding those ways. Access to public funds, so tax credits, could be a way to support particularly multifamily rental development. State and federal grants, things available through the State Division of Housing, through HUD directly, this will be different and the approach for getting those funds will be different, whether or not you're an entitlement community or a community that directly receives CDBG and/or home allocations from HUD, or if you need to work with folks at the State Division of Housing in order to access that funding. If there are any dedicated local housing funds, so, if you have a direct fund within your community that supports local affordable housing, that is going to be an incredible source to identify this gap. And then, also thinking through public-private partnerships--so, land banking, again, it's not actually dollars into the project, but changes the cost and so therefore, changes the size or the amount of the whole capital stack and therefore it's a really strategic way or tool that can be used for source. Other strategic infrastructure investments, for example, a community might decide to undertake sidewalks for a large swath of area that includes for-profit development and nonprofit development and cover the costs of the for-profit development and recoup the costs for the for-profit, but not for the nonprofit development, for example. Other cost reductions are also part of the stack. They're not part of the stack--they change the size of the stack, which then also reduces the gap as we talked about a bit with the illustration of the capital stack in previous slides.

Segment 20

At this point, we're going to turn to capital sources that are going to be available to fund your development.

Segment 21

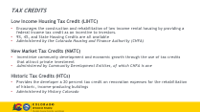

Let's start with tax credits. Tax credits come in a variety of forms. The ones we think about most commonly when we're thinking about affordable housing development are the Low Income Housing Tax Credits. Low Income Housing Tax Credits encourage the construction and rehab of low-income rental housing. And that is what they are intended to do. They come in 9% to 4%, and State housing credits all can be utilized in order to build affordable housing. In order to access tax credits, you have to work with the Colorado Housing and Finance Authority (CHFA) in order to access tax credits, and they are awarded at specific intervals. There's different timelines for each bucket of tax credits. New Market Tax Credits are a little bit different. New Market Tax Credits are to incentivize community development and economic growth so they could find commercial property, they could also find community facility, they could find a combination of commercial and community facility and housing as well. That structure can become really complicated. There might be a project that is developed with both New Markets Tax Credits, maybe the new markets utilized on the commercial side, and Low Income Housing Tax Credits used on the affordable housing development side. That is possible. It is complicated. That is always administered by community development entities. CHFA is one and could be a really good resource to start exploring but there are other community development entities that also have New Markets Tax Credits, which you can find through the US Department of Treasury CDFI website and New Markets Tax Credits information. You also have, here in the state of Colorado and all over, the Historic Tax Credits. Those are used for renovation expenses and the rehab of historic buildings. That generally is working on income-producing buildings, which could be commercial or multifamily rental, and those here in the state of Colorado administered by History Colorado.

Segment 22

From tax credits, we're going to move to federal grants. There's a variety of federal grants that are available for housing development. HUD has HOME funds. HOME, all caps, doesn't stand for anything, is the Home Investment Partnership Program, or that's what it stands for and it's the largest federal block grant to state and local governments and it's really designed to create affordable housing. HOME funds can be awarded to an entitlement area or a jurisdiction that is large enough in order to qualify for the HOME threshold. Or, if you are not in an entitlement area, you can access HOME funds through the State Division of Housing. This is similar to the process for Community Development Block Grants (CDBG). Say it three times fast and get a gold star. So, CDBG funds are designed to support community development activities. Those funds can be used for new and updated infrastructure, public facilities and installation, housing rehab, land clearance (demolition of existing buildings and creating a clear slate for new land), code enforcement, homeowner assistance, and many other things. So you might be familiar with using CDBG, for example, in your community for something like a sidewalk or traffic light project or something like that. You could think about how could you utilize CDBG in a way that can support projects like that in conjunction with affordable housing, for example, improving road or sidewalk access to an affordable housing development. We are next coming to the National Housing Trust Fund. The National Housing Trust Fund is focused on extremely low income households. So, those earning 30% or below of area median income. Colorado's Housing Trust Fund, which we have a specific Housing Trust Fund, also has an intense focus on supportive housing. That is, again, accessible through Colorado Division of Housing and working with your local development specialist on determining which of the sources is the best fit for you as you're looking at sources available from the Colorado Division of Housing.

Segment 23

So now, we're at state grants and loans. We've got, within the state of Colorado, a revolving loan fund that is administered by the Division of Housing and funds local agencies around the state as they think about single family owner occupied programs. This can be really useful if you have seniors who are aging in place and need rehab, they need a roof repair, they might need a ramp to their house, these kinds of programs might be a good fit for you and for your jurisdiction as you think about those programs (the revolving loan fund). Housing Development Loan Fund, this is also through DOLA's Division of Housing, which is created to meet and match fund requirements. So, it makes loans for developments, redevelopment or rehab--all focused on low and moderate income housing. And then we've got that Housing Development Grant Fund, often referred to as HDG, within the state of Colorado, and this is a program that provides funds for acquisition, rehab, new construction, so really many of those pieces of that capital stack. The equity that might come from the State could come from Housing Development Grant Fund, it could come from HOME, it could come from CDBG, or, if you have a specific project that might work with a loan fund, that would be the debt on that side but also be able to come from the state of Colorado through the Division of Housing.

Segment 24

State grants and loans include the Colorado Affordable Housing Preservation Fund or CAHP. The CAHP program provides acquisition financing that help you move quickly competing with market buyers. And so, this is a really interesting pot of money that can be available more quickly and more nimbly for rapid acquisition. There's also the Colorado Housing Investment fund or CHIF, which can be used in two ways. In short-term, it can use low interest loans like bridge financing which helps you secure and get your capital stack together, secure your long-term permanent financing sources. There's also short-term loan guarantees for new construction and rehab that are available through CIF. And then, you've got the Housing Development Grant fund or HDG. It's another Division of Housing DOLA program that provides funds for acquisition rehab in new construction. So basically, all of the aspects of affordable housing development can be funded through HDG. It is true that you're going to work in partnership with your housing development specialist in your region from the Colorado Division of Housing, to really think through what resources from the Colorado Division of Housing might work best to create the ultimate or final financing stack for your project. And it might be that your project is able to utilize state CDBG or state HOME plus state HDG. And maybe even, if you're thinking about acquisition or short-term financing, something from CHP, CHIF, or a revolving loan fund program.

Segment 25

So, let's get more directly into the role of local governments and a couple of examples of how local governments have played a key role in the development of affordable housing in their community

Segment 26

Let's talk about property acquisition. Local governments can be actively involved in land banking, which is the process of buying land as an investment or holding it with a designated future use specified as affordable housing. And this can be really important because again, it affects the size of our capital stack. So, it reduces the total development costs, which means it in turn, reduces the amount of debt and equity that we'll have to raise in order to build affordable housing. Another role that's really important that can be taken by local governments is property acquisition and annexation. So, should the city acquire existing land housing, mobile home communities, anything of that sort, how that is used, and if it could be donated for the purpose of rehab or redevelopment, or underwritten in some way or sold at reduced cost, that can really also reduce the capital stack and really change our developers' ability to build affordable housing in our community.

Segment 27

Let's think more through resources that can happen at a local level. We've got dedicated local housing fund creation, which provides a continuous funding stream for affordable housing. An example of that is in Summit County. Summit County voters approved a sales tax that is effective in perpetuity. Through that sales tax, now the county has its own pool of money that it can add into that capital stack and provide equity for the project. In Suffolk County, specifically, the Housing Authority receives the sales tax funds and then distributes it to each different jurisdiction within the county that needs affordable housing. Each county can do this, how they determine, and you can do this as you determine, as a local official, if you do not already have something like this in your area, determine how its distributed, how its collected, and what can be the priorities for that funding.

Segment 28

How do we leverage the local contributions? Going back to the example of Summit County, there's $76 million dollars that's been generated from the sales tax. That's a tremendous amount of money. But again, if you take it and you fund a project for the total development, it could be not that many projects at the end of the day. Specifically, thinking about how many jurisdictions we saw on that list and the previous one. So, what instead Summit County has done is taken that $76 million and leveraged it into multiple projects through either buydown programs, land banking could be a use for this money, low income housing… using it as a source in the capital stack for a Low Income Housing Tax Credit allocation and for other federal and state loan grant matches. Sometimes, there are state dollars that you get at the state level or at the federal level that require us to have local match. This kind of source is the perfect example of a source that would count as a local match. That is a way you leverage the dollars that you've earned with local contributions. It's also been realized in many places that, in addition tend to having some funds, you still want to think about different zoning opportunities and different density opportunities for affordable housing, which gets included in the reducing regulatory barriers. Also, thinking through other direct subsidies that you might be able to provide?

Segment 29

Let's talk a bit about impact and linkage fees that are directed to affordable housing. So, there's two different buckets. We've got new construction impact fee. That's a fee that's paid directly to a jurisdiction at the predetermined point of construction. So, this would be something that would happen for for-profit development. New construction for for-profit would have an impact fee that comes back to the city. That fee will then be collected and set aside for purposes of helping to fund affordable housing. There's also a commercial linkage fee. The commercial linkage fee is paid by commercial development, also impacts local housing. Typically, this fee is assessed per square foot. And so, that fee can be used directly for affordable housing around a new commercial project, for example. If there were to be a large commercial shopping area, that would be calculated per square foot and, then, that per square foot cost would help to fund, through this linkage fee, affordable housing development in the future.

Segment 30

Now, let's talk a little bit about public fee waivers. There's a variety of public fee waivers that can significantly reduce the cost of development. One that isn't often within the jurisdiction of a local municipality is wastewater and water and tap fee waivers. Those can be a huge impact on a project and, to the extent that a city or county or other jurisdiction has the ability, to help support affordable housing developers pay for those costs, or waive those costs. That could be a really important way of impacting affordable housing development in your community. Also, impact fee waivers. On the previous slide, we talked about how impact fees could be assessed, that then can be collected to support affordable housing. You also want to consider when impact fees might be able to be waived. This could be waived for affordable housing, also could be waived for schools or other development that you want to see. So, impact fee waivers. Permit fee waivers. Should you have a permitting process that has costed different milestones or multiple ways where permits are assessed... are there some of those that could be waived in order to get to the construction of more affordable housing in your community? Another set of waivers that we see as a fee in lieu of. So, if you have a fee within your organization... this is kind of an impact fee honestly, but in lieu of park, then you have to pay a fee. Right? So instead of creating public space or creating park space, you have a fee in lieu of park waiving that requirement. And the fee in lieu of requirement, maybe for affordable housing, could be an option. Not exactly a fee waiver but, on this slide, we talk also about the importance of thinking through what could be a streamlined or expedited review process for affordable housing development. So, instead of maybe having to go through all the different steps or conversations that create or allow for a lot of 'not in my backyard' or NIMBYism kind of conversation, then maybe there is a way for a more streamlined process that allows affordable housing development to go through in a more expedited way and with less cost overall associated with getting through or overcoming some of those barriers that might come up.

Segment 31

Preserving existing affordable housing. So, we've got buydown programs which allow jurisdiction to purchase favorably priced units and place a deed restriction on the property. And we also have an example of that in Summit County, which is a voluntary deed restriction program that has the goal of incentivizing homeowners to deed-restrict their property to maintain that level of affordability. It's a unique model they've got in Summit County. There's a couple of ways to think through this--if you had land bank property and then, you know, you want it to be used for for-sale, that might be a place for a deed restriction where you have either shared equity model or had it in Community Land Trust. Those are ways to think about preserving affordable housing for the long-term. Something really that needs to be considered when you're thinking about for-sale, and that's where the deed restriction can come into play, is making sure that you also have someone who can enforce and monitor that. It's very important. It can be a complicated process and sometimes can be a bit sticky. But these are all ways to think about and ensure long-term affordability for for-sale and also for multifamily rentals. So, particularly multifamily rental that was developed with any kind of incentive that was given by a local jurisdiction, could have a deed restriction or some sort of land use restriction agreement or LURA that is connected to it that ensures affordability for a certain period of time.

Segment 32

Let's talk a little bit about another case study. This is the Anvil Mount development in Silverton, Colorado. In this one, San Juan County used fees in lieu that were collected from the development of Purgatory Ski Resort or from work at the Purgatory Ski Resort for affordable housing development. Those were used to purchase the land in Silverton and then, they utilized grants from DOLA in order to build infrastructure for the project. This is unique in that they could not find an interested developer to work on this in Silverton so San Juan County acted as the developer for this project. It's also unique in that they were able to use modular design in order to get the building in the final construction. So, this building that you see on the bottom right portion of the site is built in a modular manner prefabricated and then put in place. And that allowed the county to build more economically and more quickly for their process. And with that, they needed to make sure that they had a streamline development review process, and work to put a streamline development review process in place for this and hopefully for future affordable developments as well.

Segment 33

Now, we'll look at another case study. This one is in Pueblo, Colorado, and it's called the Fuel and Iron. This is an adaptive reuse project, meaning taking an older building that had one use and then converting it into another use. In this case, this is going to become a commercial development with affordable housing on top. That's what it did become after it was a developed and put into purpose. So, that resulted in 28 affordable rental properties and then, the ground floor was a food hall and a restaurant incubator. A really cool project in Pueblo that the local jurisdiction of Pueblo, the community of Pueblo, worked closely with a developer to make happen. The way that they did that is they waived wastewater fees, which is a large cost as we talked about previously, and they provided tax increment financing or TIF financing. TIF is another really important resource that can be used in development. I do want to stress that TIF has to have, in order for tax increment financing to work, you have to have a commercial component or a component that actually is going to pay taxes or have some tax impact. So, in this case, as we discussed, it has a ground floor revenue generating space that is commercial. That's where the TIF can come into play. The other major public funding that came into this are Historic Tax Credits because it's a historic building so you can access historic tax credits, New Markets, Tax Credits, HUD funds and CDBG funds. So, again, those New Markets are key in the fact that this is a mixed-use space and it has commercial and affordable housing together. A really good and innovative project highlighting how to use multiple sources, including Historic Tax Credits, New Markets Tax Credits, and Tax Increment Financing.

Segment 34

You've reached the end of the Funding and Financing Fundamentals conversation. We want to point out some additional resources that are available to you. I'm really wanting to point you back to the Division of Housing and your development specialists who can help walk you through all the options that are available through the State of the Division of Housing. Really important. Also, please take a look at the full Affordable Housing Toolkit for Local Officials and all of the other trainings that are part of the Affordable Housing Toolkit. Some of these conversations you'll get to cover a little bit again in different conversations. The local policy toolkit is one that might be helpful or local policy training, one that might be helpful to understand some of these levers that we've used at the local level or have discussed local level today. And again, to stay updated with training materials, you can also directly contact Andrew Atchley or Natalie Wowk. We always encourage you to sign up for DOH's emails, and there is a link that will be provided for you as you access this training. Thank you for listening and I hope that you feel like you know more about the funding and financing it takes to build affordable housing.